Bad Decisions Part 1: It’s raining student loans!

When I was in college and grad school, I took out much more in student loans than I needed, to try to live above my means, and I have only recently started to understand the financial ramifications and lament the decisions that the younger Mr. SSC made. Let’s start at the best place to understand these decisions: The Beginning!

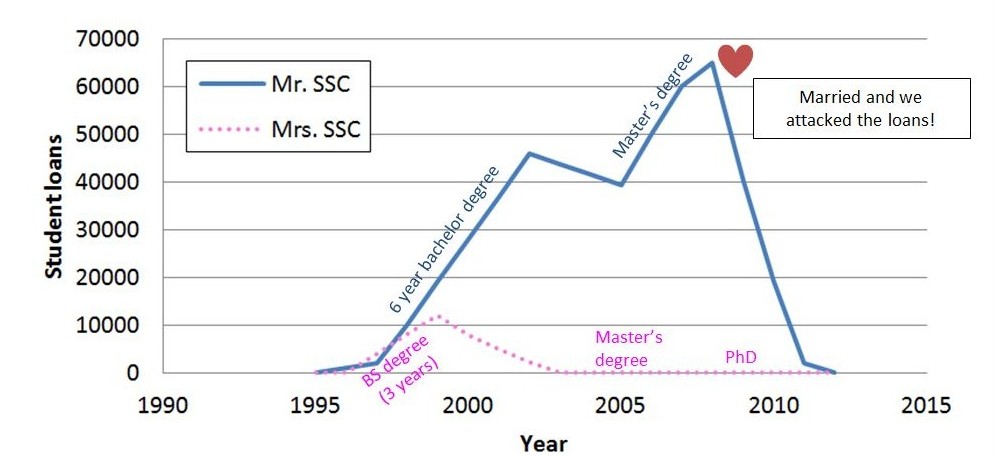

The problem started a long time ago when I was working on my Bachelor’s degree. At first, I was undeclared and attending college simply because that is what I was supposed to do. Initially, I was attending Western Kentucky University (WKU) on a Pell Grant while also working long hours at a restaurant to foot the other bills. I got the shaft when my mom married a judge and they claimed me on income tax and it derailed my Pell Grant status. After a couple of semesters paying for school myself, I took some time off to figure out what I wanted to do, and if it even involved college. My time-off resulted in a long hiking trip, and the decision to go back to school to pursue an environmental science degree. I declared my major, registered for classes, and was introduced to the wonderful world of student loans and it was amazing! They’ll “give” you money to go to school! This was brilliant! I could get a student loan, pay for school, and have some cash left over for living expenses. After all, it was ‘deferred’ – not that I really understood at the time what that truly meant. This was like getting the free money of an income tax refund two more times a year. Awesome!

Obviously, I started taking out student loans. Fortunately, the school was in-state tuition, so not very expensive. Nonetheless, I still managed to rack up about $12k in loans over my 1.5 yrs there. In August 1999, I went to Colorado to visit family and fell in love with the area. By January 2000, I was enrolled at the University of Colorado at Denver and studying full time in the geology program.

Upon transferring to CU Denver, I did myself several disservices. First, at WKU I had completed all my required elective courses, and only needed 3 semesters to complete my new major. However, CU Denver classified things differently and I needed another 30 hrs of electives (ten more classes), almost 2 whole years because I could only manage 12 hrs a semester while working. Even worse I had to take math! Two frigging yrs of math! Gah! A whole semester of trigonometry only, and a yr of algebra, and a yr of calculus and I’m sure there was a semester of regular geometry, shit, that’s 3 yrs of math, see how bad at it I am? That just added more time and $$. Second, I was now an out-of-state student subject to out-of-state tuition. This was three times the in-state tuition price. “This was fine”, I told myself, “it will only be for 2 semesters, so it won’t be that bad”. Subsequently, my school loans jumped from about $5k/semester to ~$16k/semester* for tuition alone with almost no left over funds for subsidizing living.

My plan was to live in Denver, work and go to school downtown, and be able to play in the mountains in my free time- now that’s the life! Except I now had to study a lot just to pass stupid math classes and work full time and be broke, so I didn’t get to the mountains much except to hike some 14’ers on the occasional weekend day I may have had off. Sigh…. I was maxing out loans and still working full-time at a good restaurant job, so I had that income, but no savings or contingency in case of an accident. I felt this was fine though. I was investing in me, and my future, and with this degree, surely I’d get a good job to cover these loans.

However, with my poor finance skills, I wasn’t keeping an accurate tally of how much I’d actually borrowed. Take that back, every year I got a statement that said “you owe $XX amount in student loans”, but, I’d glance at it and throw it in the trash. What I wasn’t considering was the payback. Yeah, they eventually want their money back! Gah!!! Meanwhile, I kept borrowing and taking as much as they’d give me, and it was like a breath of fresh air each semester when I’d get that check for $3-5k extra. I was so excited that I could catch up on bills, and restock my savings which was empty again (damn thing was always empty, how does that happen?). I even had a little extra money to be able to go out with friends.**

Eventually, I was out of school and had a good job as a geotechnical engineer. Yeah, I’m not an engineer, but I played one at work. It was a decent gig, I loved the job and it paid about $45,000. I was starting to live the dream baby! Then I started getting bills, a LOT of bills for my student loans. Kentucky wanted money for the WKU loan, Colorado wanted money for the CU Denver loan, and Sallie May wasn’t my friend anymore, but more like an angry ex-wife. My monthly bills were close to $500. I freaked out after covering them for 3 months when my savings died and I was still paying. I got a great rate and consolidated them all at ~2.25% interest. Hell yeah! That’s some personal financing! I cut my bill in half almost, and now just had one bill to pay, and I set it up to a separate bank account so when I overdrew my main account (yes this happened more often than not) it would still get paid. Good job Mr. SSC, let’s go out and celebrate!

I ended up going back to grad school, and got those loans in deferment as quickly as possible, whew! There’s an extra $300 a month! Now, for more student loans… Yep, I still took out student loans even though grad school tuition was paid for. I was even getting a stipend of ~$20k/yr just to go to school. But I had tasted the good life at $45k and couldn’t go back! Actually, I’m just a sucker for bad financial decisions, and I racked up another $12-15k maybe in grad school loans. See, I still don’t know… Ultimately, I was in for over $60,000 when it was all said and done.

I could have helped us get to FI and leave work to stay at home almost 2 full yeas sooner if I’d been more financially sober in my decision-making. I don’t regret the decisions I made, hell it’s what makes you the person you are – good decisions, bad decisions, ugly decisions. The main point is that by being so financially reckless in my younger days, I prolonged my work life by at least a few years.

I hope that you may be able to learn from my poor decision-making and realize that yes, you can save enough and retire early. Like early 40’s early, even with a late start in life. Hell, I made the worst of the worst decisions, and I cashed out a 401k at 28, it was up to $12000! Still, I’ve been able to recover in spite of myself. For me, it took changing my mindset of living as if there’s no tomorrow and instead looking toward a future with no work and more family time. You may want to have that time with family too, or just fishing, gardening, or doing whatever you want, but until you break that mindset of “I’ll pay it back later” it’s just not going to happen.

Let me know if you’ve made any stupid decisions you realize cost you a few more years getting to FI or early retirement. Check back for more installments of the series Bad Decisions, there have been a lot… Next up — Bad Decisions: Easy credit, hard payments.

*I tried to appeal the third semester of out-of-state tuition to have it switched to in-state, but I lost the appeal and paid the full 3 semesters out-of-state tuition, because administration loves technicalities in their favor.

** Working at a restaurant had its advantages. I got $2 pints at work (off clock, of course) and a free meal each shift (so, ~6 days a week). BUT, my friends were all servers and got $100 – $300 a night. They were always saying “let’s leave the cheap drinks here and go anywhere else to get more expensive drinks, or out to dinner, sushi anyone?”. I was running with the wrong but fun crowd, and I didn’t want to be different. So I would go and just charge it to a credit card if I didn’t have the funds available (which was always).

Even Steven

September 1, 2014Student loans creep up on you, first you are excited to go to school and like you said they are giving you money to go there, it was great. It’s a tough call would you be better off without 60K and no money lessons at all, nothing to wake you up and make you realize that you could become FI and retire early, who knows. I’m sure it would be better without student loans but maybe you don’t even think of FI if you have 5K in student loans when you are done.

Mr SSC

September 1, 2014Yeah they creep up on you. You’d think I’d have learned my lesson with the undergrad loans and not fallen back into my co-dependent relationship with Sallie Mae during grad school. But, old habits and bad relationships are hard to break. Fortunately, I did learn something along the way and they did lead to a good job, so no harm, no foul?

No Nonsense Landlord

September 1, 2014It always seems the money comes in slower than it goes out. Even in my situation, I always feel broke, as I constantly am saving, or paying bills, as fast as I can.

Keep up the great work!

Mr SSC

September 1, 2014That’s an excellent point and I’ll have to follow up with a post about it. Mainly because I still feel broke, and it sucks. How do you resolve that feeling even if you’re doing well financially, and getting ahead towards FIRE? I haven’t figured it out yet, let me know if you have any suggestions.