Bad Decisions 5: Cashing out my 401k!

Have you ever done something ridiculous like cashing out a 401k? I did. Yep, one of the biggest money mistakes you can make and I did it, against countless advice to NOT do it. Let’s go back to how this all got started.

Have you ever done something ridiculous like cashing out a 401k? I did. Yep, one of the biggest money mistakes you can make and I did it, against countless advice to NOT do it. Let’s go back to how this all got started.

The year is 2005: I had been out of college for about 3 years, had a nice steady job, and had finally gotten accepted into grad school. It was a great school with a top-notch reputation, and I would practically be guaranteed an almost 6-figure salary when I graduated. However, I was having trouble maintaining a good work/school balance. I was still working my full time construction-type job, which had pretty variable hours throughout the work week. Scheduling my job and school was a nightmare, so after a year of dealing with a harried schedule I decided school was way more important and had to be my focus. I had been going to school part-time, but since that wasn’t working out well, I bit the bullet and quit my job and signed onto school full-time. This left me with a decision to make regarding my 401k.

After looking into IRA rollovers, as well as my present bank account, I decided, “Hell, I’ll just cash it out. I can easily make up the difference when I start working again in a few years, no harm no foul. That money can help me more now.” I had applied for some student loan help already (see Bad decisions: It’s raining student loans!), but I was accustomed to living off of ~$45k a year and dropping to $20k a year as a student really hurt. I mean, I wasn’t able to keep my spending in check at $45k, so how would I do that with half the money? Realistically, I know realize that I could have made $90k and still not kept my spending in check…but that’s another story. So, I informed my company that I was going to cash it out and got some pushback. “What?!?! Don’t be stupid, just roll it over into an IRA.” “Why would you want to cash it out, you’ll get hit with taxes and penalties, you won’t even be able to keep half of it!” But I just thought, “Ha-ha! Little did they know I’d already come up with how much I’d be able to keep, and yes, with the taxes and penalties, I would not be able to keep every cent of it. BUT, here’s the kicker! I’d be able to still keep more than I put in after I cashed it out and paid it all off.” Yep, I thought I was being pretty, pretty, pretty smart. I had already calculated that the value I would get paid out, penalties and all was greater than the amount I had originally paid into my 401k… so I’d still be ahead. I was a pretty smart guy.

Even my financial person did their best to talk me out of it at the 11th hr. They even had paperwork for an IRA ready to go in case I had a moment of clarity. Did I still take the cash out? You betcha! I even had some members of my family on my side supporting my decision, because, “Hey, you need that money now. You’ll get more money once you get out of school and get a nice job.” And who am I to argue with someone that’s agreeing with me? So I cashed it out.

So, what did I do with it you ask? Surely something great and fun, and memorable because I gave up so much potential growth on that 401k, right? No, not really. As I’ve been thinking about writing this post, I realized I can’t even remember where it all went. Six years of saving for nothing!

Well, that’s not entirely true… My car’s transmission went out and instead of forking over $2k to fix it, I thought “you know what, I’m not a car guy, I need an SUV. They look cooler! Besides,I go to the mountains and snowboard and hike and fish and do outdoors stuff, of course I need an SUV.” So, I started car shopping, used of course, and something I could cover with cash, or at least just a minimum loan. I’d only had a couple of credit crads and one car loan previously, so a small car loan couldn’t hurt, right? I went out and test drove a few SUVs and haggled and got a decent deal on a 4WD Ford Explorer Sport. I loved that SUV. I’d paid most in cash, and drove off with it, while they were working up the loan details for the remaining portion. A few days later they called and said, “Well, because of your credit score not being stellar, and the fact that you don’t have a job, the banks aren’t wanting to loan you any money right now. You’re going to have to bring the SUV back or come up with the remaining portion.” Gah!!! In hindsight, I should’ve taken it back and found something I could get with the cash I put towards this deal, but no…. That’s not how young Mr. SSC thinks. Instead, I checked my bank, and what do you know, my student loans had come in, so I withdrew the remainder of the money needed and ta-da! I had my new vehicle. The rest of the 401k money went toward credit card debt, and into my meager savings account. The SUV was about the only fun thing I did with the 401k money. Man, did that Explorer turn out to be nothing but a money pit, constantly needing repairs. After only having the car for maybe 3.5 years, I traded it in for a new car – thus saying goodbye to the end of my 401k.

What I didn’t understand or calculate at the time, was the lost growth potential that my 401k could have been earning for me during those 2 years. Realistically, I wouldn’t have touched it until I was 60, if it had actually survived, so I didn’t calculate all of those earnings I would miss out on. By cashing it in, I was only counting the $8-9k I could get in the short term, which yes was more than I put into it at the beginning, so I didn’t short myself there. I was also counting on the fact that with my post grad-school job I would be able to replace that money in a year or two, so I reasoned that my 401k wouldn’t miss out on more than a couple of years growth. HOWEVER, I didn’t take into account the fact that it could keep growing and growing, from about the $12-15k it was when I cashed it out to about $45k. I wasn’t “gaining” an extra $1-2k from what I put into it, I was stealing ~$30k from my future self. Ultimately, me being “smart” cost me way more than I thought. What a moron I was. I look back on it now and shake my head that I could be so financially ignorant, but I just thought of the near future and not the retirement future, and that is what kept me thinking, “This is a good decision, and I can recover from it in no time.”

Mrs. SSC says:

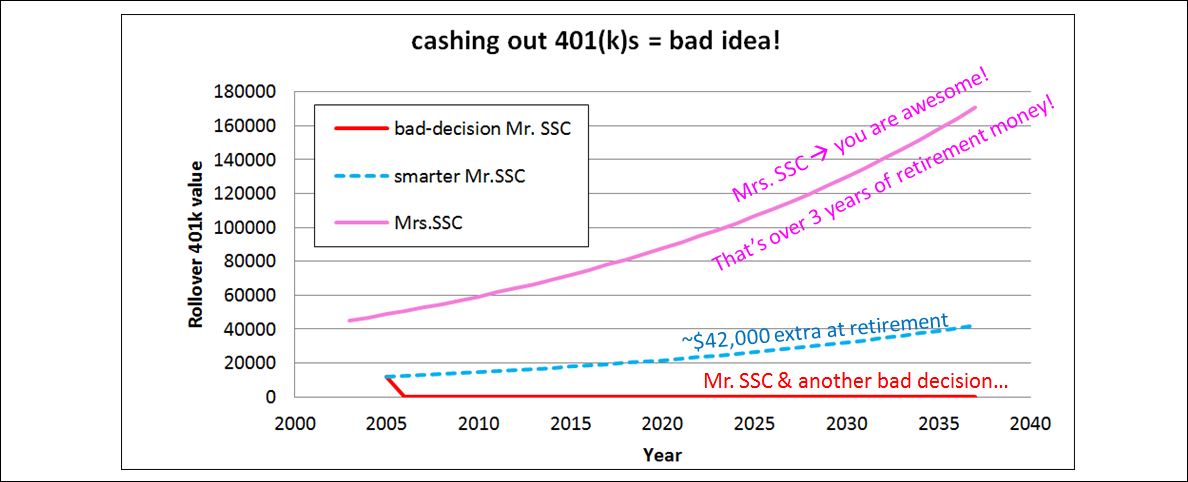

Wow! I’m beginning to realize that I don’t know even half of the stupid, bone-headed decisions Mr. SSC made when he was younger! Good thing we rushed into marriage – now we are stuck with each other! Anyways, so Mr. SSC asked me to calculate what he lost by cashing in his 401k back in 2005. Let’s say Mr. SSC cashed out $12,000 in 2005, of which he got $9,000. If instead he rolled it over to an IRA based on the advice of his coworkers, HR, and financial expert, instead of listening to his financially-backward family, who were probably just hoping that some of that money would come their way. Anyways, I’m pretending that this more intelligent version of Mr. SSC gets 7% returns, and inflation increases 3% yearly. Wow! Mr. SSC would have the equivalent of $42,000 at the time he turned 60… or about 10 months of living expenses. Looks like Mr. SSC gave up almost a year of freedom for that ‘cool’ SUV. Sigh… Just for reference, when I quit my engineering job to start graduate school in 2003, I had ~$45,000 in my 401k from about 4 years of work, which I diligently rolled over. This could grow to over $170,000 by the time we turn 60, and luckily, my good decisions should buffer Mr. SSC’s nasty financial mistakes.

What are some boneheaded money mistakes you’ve made in your life? Even better, what did you learn from them? Let me know!

CheapMom@SimpleCheapMom

September 29, 2014Well at least you’ve learned from your mistake! I think some people might think I’ve made some pretty bonehead decisions, like leaving my great job to go out on my own, then closing up shop to be a stay at home mom. I’ve definitely missed out on earnings and future growth. I don’t regret those decisions though. Not yet at least. Thanks for the great read.

Mr SSC

October 2, 2014Thanks for the comment! We hear the same stuff you did when people find out that we plan to leave our great jobs to be stay at home parents and “retired”. There are a lot of naysayers, but if you choose what’s right for you, I find that in the end it leads to being happier overall. Yes, we could keep growing our savings and retirement nest egg, while working, but trading those earnings for missing out on being more active in my kids lives is definitely not worth it to me. I’d rather take the plunge and hope for the best to be more involved with the kids.

Justin @ Root of Good

September 30, 2014Ouch!

My brother in law did the same thing at about the same time. Even the amount was about the same (around $12k, or closer to $7k after taxes). That was what he had saved in his 401k over the course of 10 years working at a blue collar job. The market has roughly doubled since then, so he would have close to $25k growing tax free year after year. Instead, he took out the $7k after taxes and blew it on dumb stuff like cheapo Christmas presents for his nieces and nephews. I’m talking mountains of cheap plastic crap. And he gambled some away and took a short weekend trip or two. The cash didn’t last very long at all unfortunately. Now he’s about to hit age 40 and just restarted a 401k and has almost nothing saved for retirement.

Good thing he has social security! 🙂

Mr SSC

October 2, 2014Even going through with it I knew it wasn’t the best idea, but I was able to rationalize it to myself at the time. While I tried to avoid spending it like your brother-in-law, or even my dad would have, it still ultimately got frittered away. Fortunately, I was able to start saving again within a year or two of cashing it out, but I still missed out on the total gains it would still be making right now if I had just left it alone. I guess some lessons you have to go through for them to sink in, but it would’ve been nice if I had just listened to anyone and left it alone. Live and learn, I suppose. 🙂

Jacq

October 31, 2015My ex took his cashed out 401k & a re-fi of his primary residence & used it towards another investment property, purchased right before the real estate bubble. He barely broke even, or had a loss. His other option with the $ was grad school that would’ve increased his earning potential. *shrug* All my 401k s roll over into Vanguard. 🙂

Mr. SSC

November 2, 2015Yeah – I made some bad choices thinking, “I’ll get it back in no time, it’s only $12k”. I shake my head how I was able to justify doing that regardless of whatever people were telling me.

Live and learn. Live and learn. Glad you roll yours over. 🙂 My last one from my previous job got rolled into vanguard, well, they already used them, and the fees were the same as our accounts (really low) so no need to do anything really.